What Are the Best Forklift Batteries? Industrial Solutions

What Are the Best Forklift Batteries?

James Mitchell

January 8, 2025

Anyone asking this question in 2025 and still considering lead-acid for a multi-shift operation has not done the math.

The short answer: LFP lithium. Specifically, from a manufacturer that actually specializes in forklifts rather than selling the same cells they put in golf carts with different marketing.

The longer answer requires understanding why lead-acid refuses to die despite being objectively worse in almost every measurable way for serious operations.

Why Lead-Acid Still Exists at All

Lead-acid technology peaked decades ago. The chemistry cannot improve further. Sulfuric acid and lead plates doing their electrochemical dance the same way they did in 1890.

The 8-8-8 rule governs every lead-acid battery: eight hours running, eight hours charging, eight hours cooling. Break this rule through opportunity charging and watch sulfation destroy the plates within two years instead of five. Sulfate crystals form on the plates as the battery discharges. A complete charge cycle dissolves those crystals back into the electrolyte. Interrupt that process repeatedly and the crystals harden permanently. Battery capacity drops. Charging times stretch longer. Eventually cells fail one by one until the whole pack becomes scrap.

The training consists of "plug it in at night, check the water sometimes." That level of instruction might have worked in 1985 when battery technology matched the simplicity of the training. Modern operations with multiple shifts and pressure to maximize uptime break every rule that lead-acid chemistry requires. The batteries suffer. The operations suffer. Everyone blames the wrong things.

Maintenance adds insult to injury. Weekly watering, monthly equalization, constant terminal cleaning. Miss the watering schedule and plates dry out. Overwater and acid overflows during the next charge, eating through concrete floors and anything else in its path. The timing matters too. Water goes in after charging, never before. Add water before charging and the expanding electrolyte spills everywhere.

The vendors selling lead-acid rarely mention how often facilities screw up equalization. Most chargers have an equalize function that nobody uses correctly. The button sits there. Operators ignore it. Maintenance schedules say monthly equalization but production pressure means skipping it becomes routine. Six months later, capacity has dropped fifteen percent and everyone blames the battery instead of their own negligence.

Equalization stirs the acid back together through controlled overcharging that creates gas bubbles.

Acid stratification explains why so many batteries die at three years instead of five. The purchasing manager blames the vendor. The vendor blames the maintenance crew. The maintenance crew blames the operators.

The maintenance crew turnover makes everything worse. New guys come in with no training on battery care. Old guys leave without documenting what they knew. Institutional knowledge evaporates every time someone quits or gets promoted or transferred. The batteries pay the price for organizational dysfunction that has nothing to do with battery technology.

The weight argument remains the only honest defense of lead-acid. Those 2,000-plus pounds serve as counterbalance during lifting. Lighter lithium packs sometimes need added ballast. Fair point. But weight alone cannot justify everything else lead-acid forces operators to tolerate.

Crown Makes the Best Lead-Acid Battery and Everyone in the Industry Knows It

Crown Battery operates out of Fremont, Ohio. Nearly a century in business. The CoolFlow thermal management system genuinely works in high-temperature environments where cheaper batteries cook themselves from the inside out.

Warehouse managers running Crown V-Line packs report seven-plus years of service even with maintenance lapses that would kill lesser batteries faster. The five-year warranty means something because Crown actually honors claims without fighting. Try getting GNB or one of the offshore brands to honor a warranty claim. Good luck. Hours on the phone arguing about whether the failure resulted from defective materials or operator error. Documentation requirements that seem designed to deny claims rather than process them. Crown just fixes the problem and moves on.

The price premium Crown charges over generic alternatives pays for itself in extended service life and reduced hassle. Purchasing agents who beat up vendors for discounts and end up with off-brand batteries discover the savings evaporate when those batteries fail early and need replacing. Penny-wise, pound-foolish purchasing remains endemic in this industry. The guy approving the PO never has to deal with the dead battery at 2am when the night shift needs to move product. He just sees the lower number on the invoice and calls it a win.

Crown costs more. Crown lasts longer. Crown causes fewer headaches. The math works out in Crown's favor for anyone patient enough to track actual battery performance over five years.

This pattern repeats across every facility that tries to save money on batteries. Year one looks great. Costs came in under budget. Year two the problems start. Capacity dropping faster than expected. Unexpected failures during peak periods. Year three the whole fleet needs replacement and the total cost exceeds what Crown would have charged in the first place.

Deka from East Penn runs close behind Crown. The 3M internal study ranking Deka first carries weight because 3M buys enormous quantities and has no reason to favor any vendor. Quality control at their Pennsylvania facility maintains consistency that offshore competitors struggle to match. Deka lacks some of Crown's thermal management sophistication but compensates with solid construction and reliable performance across typical operating conditions.

Everything else in lead-acid blends together in the middle. GNB works fine. Hawker works fine. The various house brands that dealers push work fine. Fine meaning adequate performance with adequate maintenance until adequate becomes inadequate and the battery dies at year three instead of year five. The real differentiator becomes local dealer support rather than the battery itself. A responsive dealer with parts inventory and service technicians matters more than which name appears on the case.

The lead-acid vendor market frustrates buyers seeking clear distinctions. Sales representatives for every brand make identical claims about quality and service. Spec sheets look similar. Warranties offer similar terms on paper even though enforcement varies wildly. Without field experience across multiple brands, the selection process becomes guesswork. And most purchasing managers lack that field experience because their job involves buying stuff, not operating stuff.

Crown costs more. Crown lasts longer. Crown causes fewer headaches. The math works out in Crown's favor for anyone patient enough to track actual battery performance over five years instead of just comparing invoice prices in a spreadsheet. But most people never track that data. They just buy whatever the vendor quotes cheapest and then complain when batteries die early. The complaints go to the maintenance department. The maintenance department gets blamed for poor battery life. Nobody questions the original purchasing decision that set up the maintenance department for failure.

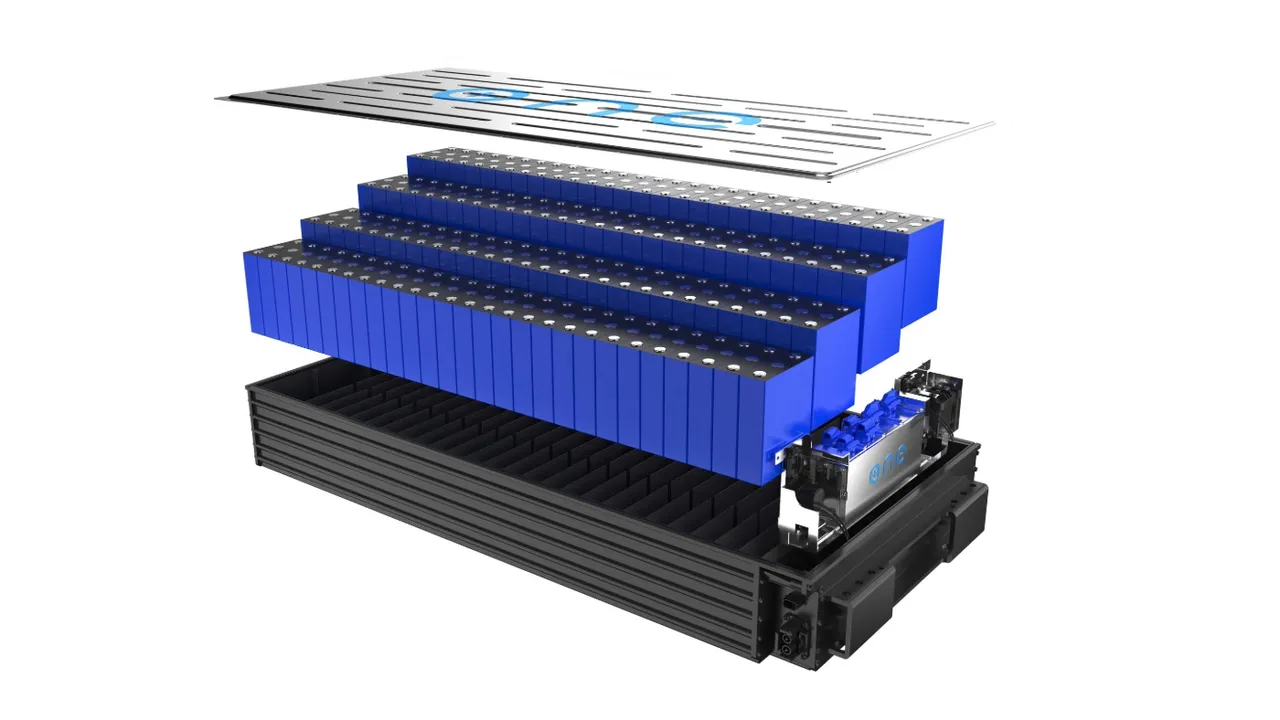

LFP Lithium Changed Everything and Most Operations Still Have Not Caught Up

Lithium iron phosphate chemistry changed the economics permanently. Not because of any single advantage but because the advantages compound.

Charging efficiency sits around 95% versus the 75% range for lead-acid. That gap means less electricity purchased for the same work output. Multiply across a fleet running year after year and the dollars add up. Nobody tracks electricity costs by battery type. The utility bill just shows total consumption. But the differential exists whether anyone measures it or not.

Cycle life extends to several thousand charges versus maybe 1,500 for well-maintained lead-acid. Poorly maintained lead-acid might give 800 cycles before capacity drops below useful levels. The math on replacement frequency alone tilts the TCO calculation toward lithium for any operation running more than single shifts.

LFP lithium technology offers charging efficiencies and cycle life that fundamentally change the economics of fleet operations

Opportunity charging works with LFP. Plug in during lunch. Plug in during shift change. Plug in whenever convenient. The chemistry handles partial charges without penalty. One battery per forklift, charged opportunistically, replaces the entire infrastructure of spare batteries, changing rooms, extraction equipment, and cooling schedules that lead-acid demands.

That infrastructure elimination deserves more attention than it gets. Multi-shift lead-acid operations need dedicated battery rooms. Not small rooms either. Space for spare batteries, charging stations, ventilation systems to handle hydrogen gas during charging, containment for acid spills, extraction equipment to swap batteries, traffic lanes for battery carts. All that square footage contributes nothing to revenue. Warehouse space costs money. Every square foot devoted to battery handling could instead store inventory or support operations.

Voltage holds steady throughout discharge with LFP. Lead-acid voltage sags progressively as charge depletes. A forklift lifting 3,500 pounds at shift start might struggle with 2,600 pounds by afternoon. Operators feel the machine getting sluggish. They assume the battery needs charging. They interrupt their work. The productivity loss adds up across shifts and weeks and months. LFP maintains flat output until nearly depleted. Full power until the BMS says stop.

Flux Power for Large Fleets, Chinese Manufacturers for Everyone Else

For lithium, the brand question gets complicated by the gap between premium and budget options.

Flux Power operates from Vista, California with exclusive focus on material handling applications. The documented case studies showing million-dollar annual savings represent real operations, not marketing fiction. The engineering team understands forklift-specific problems that general battery manufacturers overlook. Integration with fleet management systems works properly. BMS calibration matches actual usage patterns.

Premium: Flux Power

Best for large fleets where per-unit cost difference becomes negligible against operational savings. Superior engineering, fleet management integration, and BMS calibration optimized for material handling. Premium pricing justified at scale.

Value: BSLBATT & ROYPOW

Chinese manufacturers offering legitimate alternatives at lower price points. Certification packages confirm safety compliance. Quality has improved dramatically over the past five years. Best for operations with in-house technical capability.

Flux charges premium prices. Large fleets absorb that premium because the per-unit cost difference becomes negligible against operational savings. Smaller operations with tighter budgets may find the pricing difficult to justify despite the performance advantages. The ROI calculation favors Flux strongly at scale but weakens for operations with only a few trucks.

BSLBATT and ROYPOW from China offer legitimate alternatives at lower price points. The certification packages confirm safety compliance. Quality has improved dramatically from Chinese manufacturers over the past five years. The stigma attached to Chinese batteries reflects outdated experience rather than current reality. The cells come from the same factories supplying everyone else. The BMS sophistication has caught up with western competitors.

The Chinese manufacturers struggle with service and support infrastructure in North America. Shipping replacement parts from Shenzhen takes weeks. Technical support operates across time zones and language barriers. For operations with in-house technical capability, these limitations matter less. For operations dependent on vendor support, the lower purchase price may create headaches that exceed the savings.

Toyota, Linde, and other OEM lithium packs work without compatibility issues on their respective forklifts but carry premium pricing that independent alternatives can undercut significantly. The OEM approach makes sense for fleet managers who want single-vendor accountability and simplified procurement. Independent alternatives make sense for fleet managers willing to manage multiple vendor relationships in exchange for cost reduction.

Nobody talks about the middle market. Operations too large for budget batteries but too small for Flux pricing. That segment ends up choosing between overpaying for OEM packs or gambling on Chinese alternatives without adequate support. The market has not yet produced a clear winner for mid-sized fleets.

Cold Storage Is a Different Game Entirely

Freezer and refrigerated warehouse operations eliminate lead-acid from consideration entirely. The chemistry simply fails in cold environments.

Lead-acid capacity drops roughly 25% at refrigerator temperatures. In freezer conditions around -18°C, capacity loss reaches 50% or worse. A battery sized for eight hours delivers four. Maybe five with careful management. The physics cannot be engineered around. Cold electrolyte moves sluggishly. Ion transfer slows. No amount of better plate design changes the fundamental temperature sensitivity.

Cold storage environments present unique challenges that eliminate lead-acid technology from serious consideration

Charging compounds the problem. Cold lead-acid absorbs charge slowly and incompletely. Best practice requires pulling forklifts out of cold zones to ambient-temperature areas for charging. The transition creates condensation. Water droplets form on cold metal surfaces when warm air hits them. Those droplets penetrate connectors, relays, and motor housings. Corrosion develops in places nobody can see until failures occur.

Building heated battery rooms adds infrastructure cost on top of operational hassle. The battery room needs climate control. Doors need air curtains or vestibules. Staff need to move batteries back and forth rather than charging in place.

LFP with proper cold-weather engineering maintains near-full capacity at temperatures that cripple lead-acid. The key phrase being proper engineering. Generic lithium packs without heating systems, insulation, and moisture protection will also fail in freezers. Purpose-built cold storage batteries from ROYPOW and BSLBATT address these requirements with active thermal management. The heating systems draw power from the battery itself, creating parasitic load that reduces effective capacity slightly. The tradeoff remains strongly favorable compared to lead-acid alternatives.

Toyota claims their cold storage lithium variants operate continuously at -30°C with integrated heating. Field reports confirm this works in practice. Forklifts running entire shifts in freezer environments without the temperature transitions that destroy equipment and waste operator time.

The NMC Question

Some lithium manufacturers push NMC chemistry, emphasizing energy density and lighter weight. For forklifts, these claims miss the point.

Energy density matters for vehicles where range depends on minimizing weight. Forklifts operate in defined areas with charging available. The battery compartment size stays fixed regardless of chemistry. Lighter weight actually creates problems by reducing counterbalance effectiveness.

NMC enters thermal runaway at lower temperatures than LFP. Warehouse fires from battery failures make headlines and destroy businesses. LFP provides a safety margin that carries genuine value.

Cycle life favors LFP substantially. Testing at Sandia National Laboratories found LFP outlasting NMC under equivalent conditions. At deep discharge cycles, the gap widens further.

Cold performance remains the single legitimate NMC advantage. Below -10°C, NMC maintains capacity better without preheating. But competent LFP manufacturers solved this years ago with integrated heaters.

The Mistakes Everyone Makes

Sulfation kills more lead-acid batteries than any other cause. The mechanism operates invisibly until damage becomes irreversible.

Opportunity charging on lead-acid accelerates sulfation because charges never complete. Fleet managers who allow operators to grab quick charges between tasks because it seems efficient discover within two years that their battery fleet needs premature replacement. The same managers then blame the battery vendor for selling them defective product. The vendor points at the charging logs showing hundreds of partial charges. The argument goes nowhere. The batteries still need replacing.

Critical Insight

Opportunity charging only works with lithium chemistry. Lead-acid needs complete charge cycles. Implementing opportunity charging practices on lead-acid fleets will destroy battery life within two years—a costly mistake that stems from misapplying lithium-era practices to legacy technology.

This happens constantly. A new fleet manager reads about opportunity charging being the future of battery technology. He implements it without understanding that opportunity charging only works with lithium chemistry. Lead-acid needs complete charge cycles. Nobody told him. Or someone told him and he ignored it because the lithium salesman's pitch sounded convincing. Two years later the facility has burned through a battery fleet that should have lasted five years and the fleet manager has either learned an expensive lesson or moved to a different job before the consequences caught up.

Chronic undercharging produces the same result more slowly.

Temperature abuse operates through different mechanisms. Lead-acid suffers accelerated corrosion above 77°F. Every 15-degree increase roughly halves battery life. Warehouses in southern climates without environmental controls routinely operate at temperatures that destroy batteries in half their rated lifespan. Nobody tracks this failure mode because the batteries appear to age normally, just faster than expected. The maintenance manager blames the battery vendor. The vendor blames maintenance practices. Both miss the temperature problem hiding in plain sight.

The temperature issue frustrates everyone involved because the damage looks exactly like normal aging. Nothing visible changes. The battery just wears out faster. Without temperature logging showing sustained operation at 95°F or higher, nobody can prove the operating environment caused premature failure. The vendor cannot be blamed. The maintenance crew cannot be blamed. The purchasing decision cannot be blamed. Everyone shrugs and orders replacement batteries and the cycle continues.

Charger mismatch causes damage that accumulates invisibly over hundreds of cycles. Using a charger rated higher than battery specifications causes gassing, overheating, and accelerated wear. Using one rated lower prevents full charging and promotes sulfation. Facilities with mixed fleets where operators grab whatever charger sits closest create systematic damage across their battery inventory. The damage manifests as shortened battery life attributed to manufacturing defects or poor maintenance rather than the actual cause.

LFP batteries tolerate abuse better but face their own vulnerabilities. Charging below freezing can plate lithium metal onto anodes, permanently reducing capacity. Quality BMS systems prevent this by refusing charge commands at unsafe temperatures. Cheap batteries without proper BMS protection suffer damage that operators may not recognize until capacity loss becomes severe.

The Hidden Cost Problem

The purchase order shows battery price. It does not show maintenance labor. Lead-acid demands weekly attention. Watering, cleaning, monitoring. Figure 50-60 hours annually per battery for a responsible maintenance program. Multiply across a fleet. LFP requires essentially nothing beyond visual inspection.

The purchase order does not show infrastructure costs. Multi-shift lead-acid operations need battery changing rooms with extraction equipment, ventilation for hydrogen gas, containment for acid spills. That floor space has alternative value. The battery room contributes nothing to revenue.

The purchase order does not show energy waste. The charging efficiency gap between lead-acid and LFP translates directly to electricity bills. Nobody tracks electricity costs by battery type. The differential exists whether anyone measures it or not.

The purchase order does not show replacement frequency. Lead-acid lasts three to five years with proper care. LFP lasts ten to fifteen. Over a long planning horizon, the replacement cycles accumulate.

The purchase order does not show downtime costs. Battery swaps, charging delays, and failures reduce forklift availability. Operations relying on lead-acid accept availability losses that LFP operations avoid.

Purchasing managers evaluating only invoice prices make decisions that cost their employers substantially more than the apparent savings. The CFO sees lower capital expenditure. The operations manager sees higher operating costs eating that savings and then some. The disconnect between procurement metrics and operational reality persists across the industry because the people buying batteries never have to operate with the batteries they bought.

The Actual Decision

Single-shift operations with tight budgets can reasonably choose Crown or Deka lead-acid. The 8-8-8 cycle fits natural rhythms. Overnight charging completes before morning shift. Maintenance requirements stay manageable for smaller fleets. The lower invoice price matters when capital constraints dominate.

Multi-shift operations should not be considering lead-acid at all. The TCO calculation favors LFP within three years under typical usage. Operational benefits begin immediately. The higher purchase price represents investment rather than expense.

Cold storage operations have no choice. LFP with cold-weather engineering or failure. Lead-acid cannot perform in freezer environments regardless of brand or maintenance quality.

The technology question resolved years ago. Market adoption lags because purchasing decisions follow inertia rather than analysis. Operations still running lead-acid in multi-shift environments subsidize competitors who made the switch and captured the resulting cost advantages.

Crown for lead-acid. Flux for large lithium fleets. BSLBATT or ROYPOW for smaller lithium fleets willing to manage support limitations. OEM packs for operations wanting single-vendor simplicity at premium pricing. Those are the answers. The question was never difficult.

◆

The technology question resolved years ago. Market adoption lags because purchasing decisions follow inertia rather than analysis.