Lithium iron phosphate. That covers about 80% of commercial trucks shipping today. The eActros 600, the Volvo electric trucks, the Freightliner eM2, all running LFP cells.

Five years ago nobody predicted this. The industry consensus was that trucks would need maximum energy density, which meant nickel chemistries. Consultants wrote reports explaining why. OEMs planned product lines around it. That consensus turned out to be completely wrong, and the reasons are more interesting than the usual "LFP got cheaper" explanation.

electric trucks charging at a logistics depot

The Cycle Life Math That Changes Everything

I keep seeing articles that compare LFP and NCM on energy density, then move on like that settles the question. It does not settle anything for commercial trucks.

A delivery truck for a company like Sysco or McLane runs maybe 120 miles a day. Back to the depot every night. Plugs in. Does this five days a week, fifty weeks a year. Call it 250 cycles annually. Over ten years that is 2,500 cycles.

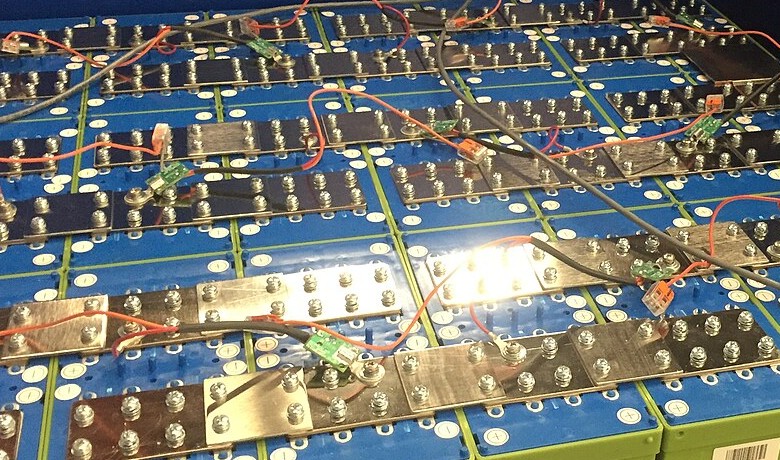

NCM batteries from LG, Samsung, and SK typically hit 80% capacity somewhere in the 1,000 to 2,000 cycle range. Truck needs a new pack around year five, maybe year six if the driver is gentle with it. Replacement cost for a 350 kWh pack runs forty-something thousand dollars once you add labor. On a truck that cost 160 grand new, this is brutal.

LFP from CATL or BYD? The cells test at 3,500 cycles minimum. Good batches hit 5,000. The truck runs its entire ten-year service life on the original battery.

You can talk about energy density all day. The fleet manager in Memphis is looking at a spreadsheet showing $45,000 in avoided battery replacement. That is the conversation that actually happens in purchasing meetings.

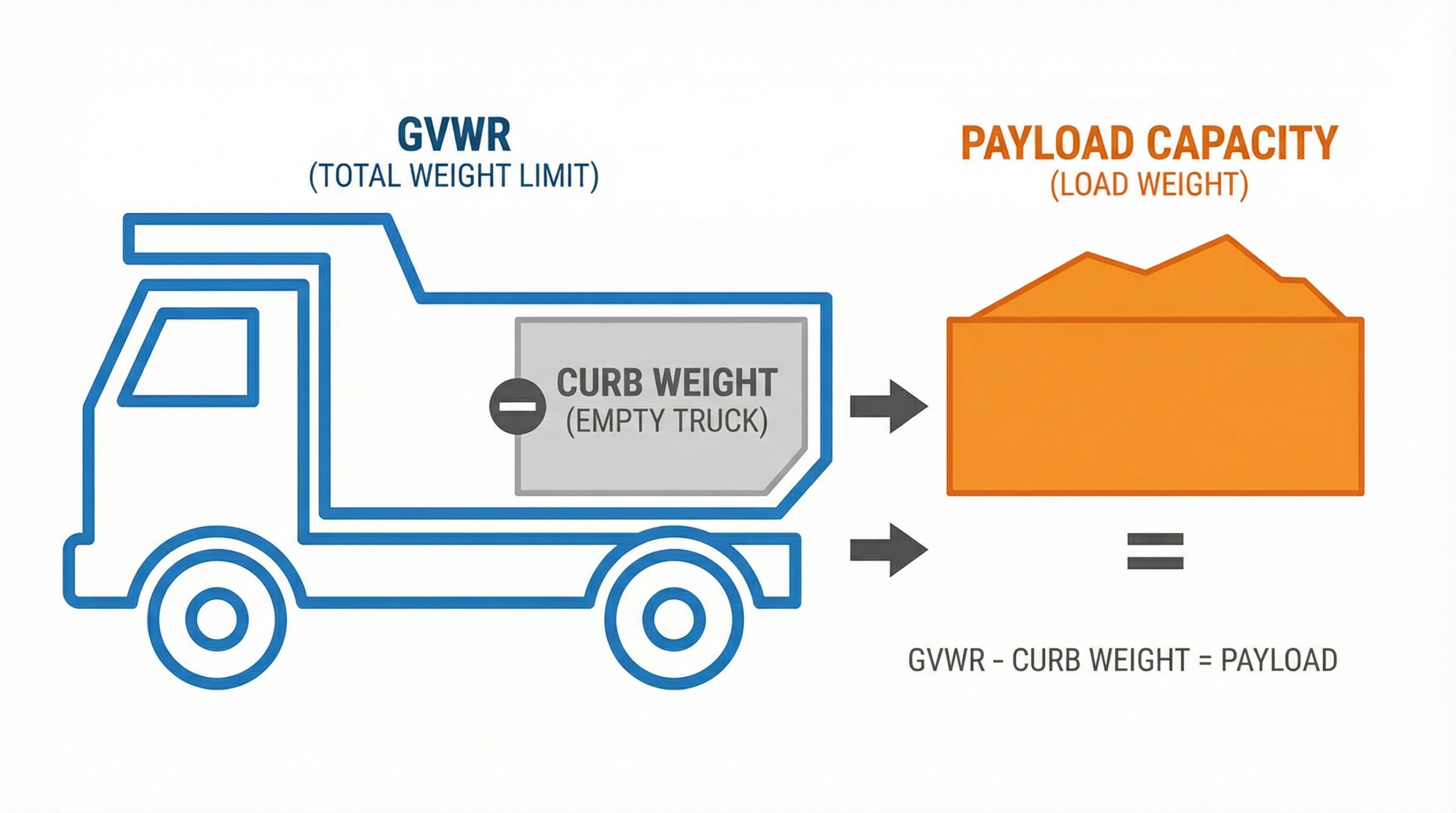

Weight Penalty Is Real But Overstated

The energy density gap between LFP and NCM is real. Around 170 versus 270 watt-hours per kilogram depending on whose cells you are measuring. For a 500 kWh truck battery, the LFP version weighs something like a thousand kilograms more.

Sounds like a dealbreaker until you think about what trucks actually haul.

Commercial delivery fleets typically hit volume limits before weight limits

UPS and FedEx trucks fill up with boxes. Amazon vans, same thing. The cargo compartment hits maximum volume while legal weight capacity sits unused. Adding a thousand kilos of battery weight changes nothing about operations because the constraint was never weight.

Restaurant supply trucks from Sysco and US Foods operate similarly. Produce, frozen goods, cases of napkins. Volume fills before weight.

The applications where battery weight directly reduces payload are specific. Cement trucks. Tankers. Flatbeds hauling steel plate. These trucks carry dense material where you actually use the full weight rating. But what percentage of total trucking is that? Industry data suggests bulk commodity transport is maybe fifteen or twenty percent of commercial vehicle miles. The other eighty percent hits volume limits first.

European regulators figured this out, which is why EU rules now let electric trucks exceed standard weight limits by four tonnes. Explicit acknowledgment that penalizing battery weight makes no policy sense.

Tesla Semi Exists in a Strange Limbo

The Semi specs are genuinely impressive. Nine hundred kilowatt-hours of battery. Five hundred miles of range with a full load. The 4680 cells that Tesla spent years developing.

Tesla announced this truck in 2017. It is now 2025 and production volumes remain modest. The PepsiCo trucks from the initial delivery still show up in every press release. When a manufacturer keeps recycling photos of the same customer vehicles for three years running, you can draw your own conclusions.

Long-haul trucking for electrification

Part of this is the 4680 cell ramp. Tesla manufactures these internally and the yields reportedly took longer than planned to stabilize. Internal production costs are rumored to be double what CATL charges for equivalent NCM cells. On a 900 kWh pack that is a lot of extra cost.

But the deeper issue might be market fit. Who actually needs 500 miles of range in a truck?

American hours-of-service rules cap driving at eleven hours. Add mandatory breaks and practical daily distance tops out around 550 miles even for drivers pushing hard. A truck with 300 miles of range that charges during a lunch break covers the same ground as a 500-mile truck that never stops. The 500-mile truck just carries three hundred extra kilowatt-hours of battery it does not use most days.

The Megacharger network that would make those 500 miles useful barely exists. Tesla has maybe a handful of locations. The regular Supercharger network cannot physically accommodate a Semi.

Meanwhile Mercedes shipped the eActros 600 with 621 kWh of LFP and 310 miles of range, designed to last 1.2 million kilometers. Less exciting specs, but actually optimized for how regional trucking works. The purchasing manager at a logistics company cares about predictable ten-year economics, not maximum theoretical range.

Medium Trucks Just Work

Freightliner eM2. Volvo FL Electric. Peterbilt 220EV. BYD T7. These are not pilot programs anymore. They are revenue-generating trucks in commercial fleets.

The duty cycles in this weight class match current battery technology almost perfectly. Routes of 80 to 140 miles. Return to depot nightly. Eight to twelve hours to charge. A 250 kWh LFP pack handles this with margin to spare.

Refuse trucks benefit significantly from regenerative braking

Refuse trucks might be the best application of all. The Mack LR Electric does constant stop-and-start driving at every house and every dumpster. Regenerative braking recovers a huge percentage of energy on these routes, something like a quarter of total consumption. The New York sanitation department has been running them for a couple years now and reports they spend almost nothing on brake maintenance compared to diesel trucks. The pads last forever when regen does most of the stopping.

The numbers are boring in exactly the way fleet managers like. Predictable costs. Known maintenance intervals. None of the excitement of bleeding-edge range achievements. Just trucks doing truck things reliably.

What Rivian and Ford Learned About Pickups

Rivian did something interesting for the 2025 R1T. The base model switched from NCM to LFP. Less range, around 270 miles, but lower price. The expensive trims kept NCM for buyers who want maximum capability.

Two years of sales data apparently taught Rivian that most pickup buyers do not need four hundred miles of range. They need a truck that costs less. The LFP base model lets Rivian offer that.

Ford's lesson was harsher. The F-150 Lightning launched to strong initial demand, but by late 2025 Ford announced it would kill the product and develop a thirty-thousand-dollar electric pickup instead. The Lightning cost too much. Ford concluded that price matters more than range for the mass market.

The next Ford electric truck will almost certainly use LFP. Range will drop. Ford is betting most buyers will not care.

Stellantis went even further with Ram. They cancelled the pure-electric 1500 REV entirely. The production version uses a 92 kWh battery plus a gas engine as a generator. You get 145 miles of electric range and 690 miles total. Maximum towing capacity is fourteen thousand pounds.

This seems like a retreat, and maybe it is. But Stellantis clearly decided that battery technology cannot yet solve the towing problem. Pulling a trailer doubles or triples energy consumption. A truck rated at 300 miles delivers a hundred when you hook up a boat. The range-extended architecture gives those buyers a safety net that pure-electric cannot match today.

Solid-State Is Not Coming When They Say

Toyota says 2027. They said 2025 a few years ago. They said early 2020s before that.

QuantumScape raised billions on prototype performance. Volume manufacturing remains unproven. The pilot line they keep talking about has not shipped commercial quantities.

BMW says 2030 now. That date will probably move too.

The laboratory results are real. Solid electrolytes enable energy densities that would change everything if you could manufacture them at scale. The "at scale" part is where every program has stalled for fifteen years.

Toyota's approach uses sulfide compounds that react badly with air and moisture. The manufacturing environment requirements are extreme. The repeated timeline delays suggest these problems remain unsolved.

For anyone making fleet decisions, treat solid-state as a post-2030 technology. Maybe later. Definitely not 2027.

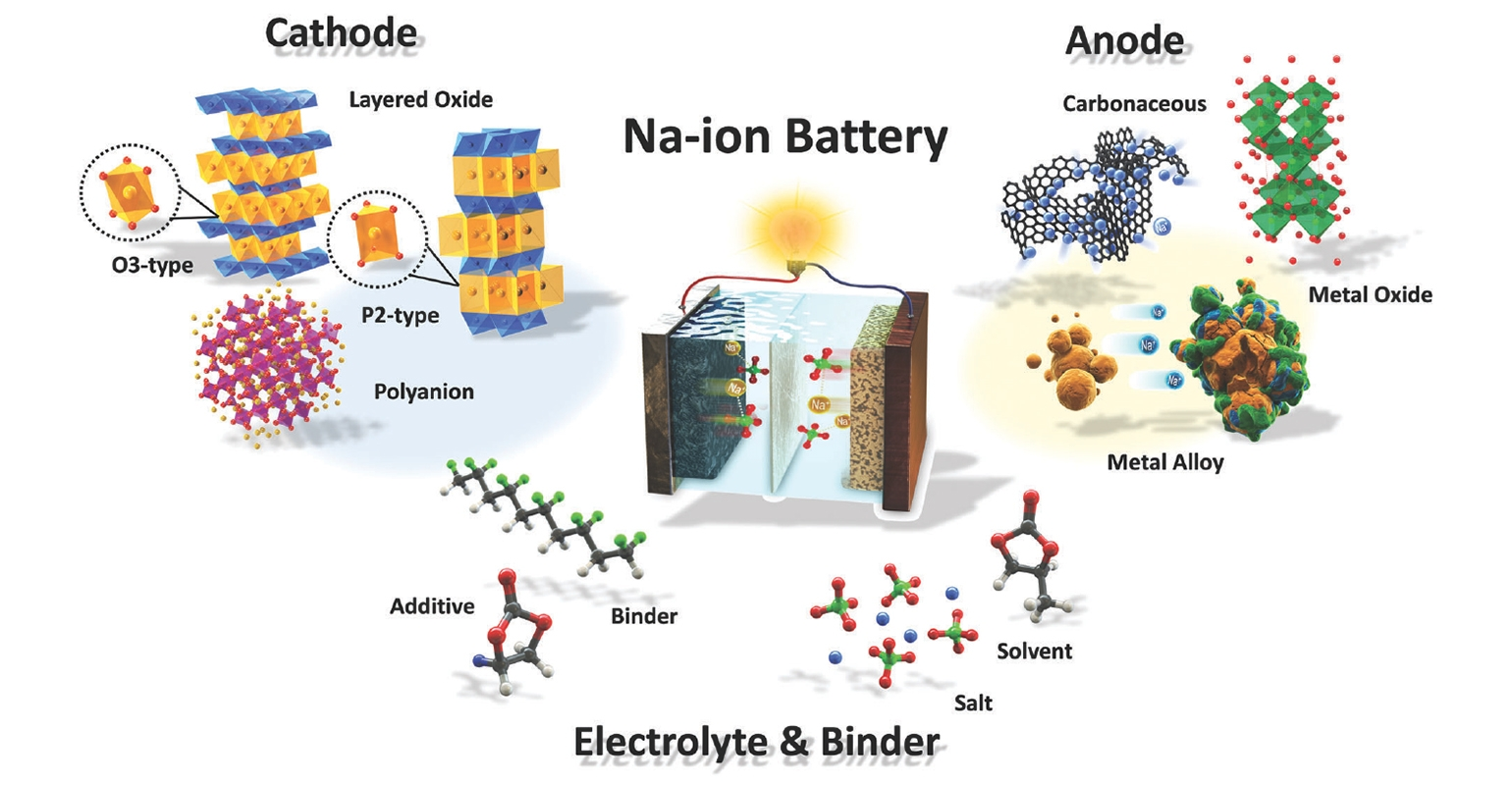

Sodium-Ion for Specific Situations

Sodium cells have reached early commercial production. The chemistry uses sodium instead of lithium and costs almost nothing since sodium is basically table salt feedstock.

Energy density is the catch. Current sodium-ion runs about 160 to maybe 190 watt-hours per kilogram, similar to LFP. You are not getting long range from this chemistry.

Sodium-ion technology offers promise for specific applications

What you might get is a cheap battery for trucks that do not need long range anyway. Urban delivery running fixed hundred-mile routes. The vehicle fills with packages before the battery runs out. If sodium-ion costs thirty or forty percent less than LFP at scale, and that seems achievable given raw material costs, the economics could work for these applications.

Cold weather is the other angle. Lithium batteries hate cold. Below freezing, capacity drops off a cliff. Sodium-ion keeps working down to minus forty. Fleet operators in the upper Midwest or Scandinavia deal with months of degraded lithium performance. Sodium-ion might genuinely be better in those markets.

Probably two or three years before this is a real purchasing option in North America or Europe. Worth watching but not worth waiting for.

Supply Chain Is the Actual Risk

CATL makes about 38% of the world's EV batteries. Add BYD and two Chinese companies account for over half of global production. CATL supplies Mercedes, BMW, Volvo, Volkswagen.

The US government designated CATL as a Chinese military-linked company. No sanctions yet, but the designation exists. If US-China relations deteriorate further, battery supply to Western automakers could be disrupted.

The Inflation Reduction Act throws money at domestic production. The credits run $45 per kilowatt-hour for manufacturing. Factories are under construction in Georgia, Tennessee, Michigan. But building and ramping battery plants takes years. The supply chain will remain concentrated through at least 2028.

For fleet buyers, this affects vehicle availability more than vehicle choice. Manufacturers with tight battery supply have tight truck production. Delivery timelines stretch. Large fleets get priority allocation. Smaller operators may find some models simply unavailable regardless of what they want to order.

Making a Decision

- LFP for daily-cycling commercial trucks. The cycle life advantage ends the debate. Urban delivery, regional distribution, refuse, food service. LFP handles all of it.

- NCM for long-haul applications where range matters enough to pay for it. A real market exists here. Smaller than the attention it gets.

- Sodium-ion eventually for cold weather and ultra-low-cost urban applications. A few years out.

- Solid-state in the 2030s if ever.

Waiting for better technology would be a mistake. The trucks available today work for most applications. Operating cost advantages accumulate from day one. Competitors deploying electric trucks now build experience and savings that cannot be quickly replicated. The reasonable choice is to buy what works today, not to wait for announcements that keep getting pushed back.