Why Southeast Asia Is Becoming a Lithium Battery Manufacturing Hub

Energy & Infrastructure

Why Southeast Asia Is Becoming a Lithium Battery Manufacturing Hub

Long-Form Analysis

Southeast Asia is becoming a lithium battery manufacturing hub because Indonesian nickel and Chinese capital needed each other within the same five-year window, and ASEAN’s trade architecture provided the legal shell for that marriage. Everything else annotates these three forces.

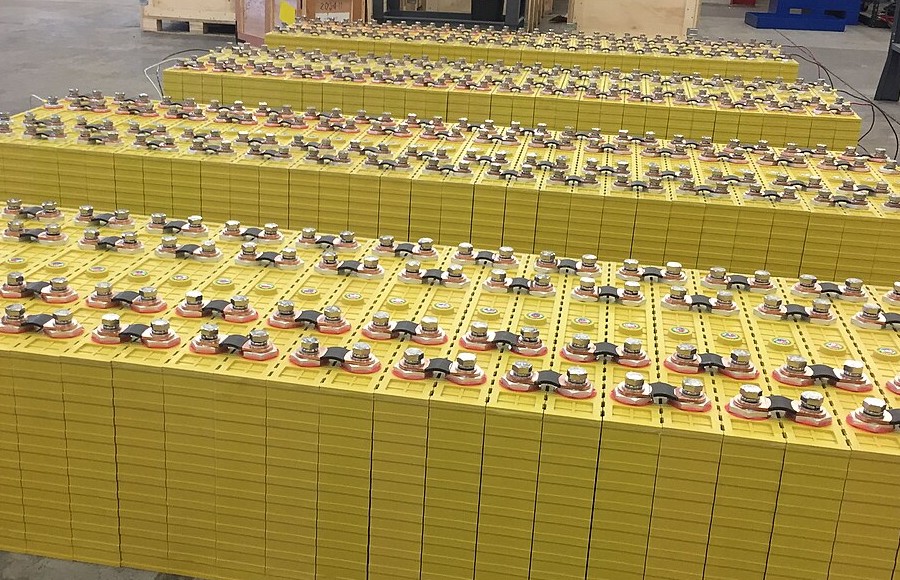

Indonesian laterite nickel operations on Sulawesi

Nickel Is the Entire Story

The battery is called a “lithium” battery, which has misdirected public attention for years. Chile, Australia, and Argentina fight over lithium deposits while cameras roll. That fight matters less than people think. Inside the cathode cost structure of an NMC811 cell, nickel accounts for a far greater share than lithium does. Lithium carries the electrochemical reaction. Nickel sets the ceiling on energy density. Whoever controls nickel supply has a chokehold on every high-end cathode material producer on the planet.

Indonesia sits on roughly half of all proven nickel reserves on Earth. The geology here dictates everything downstream. Indonesian nickel is laterite ore, not the sulfide deposits at Sudbury in Canada or Norilsk in Russia. Sulfide nickel ore can be processed by conventional pyrometallurgy, flash smelting in a furnace, a process so well-understood that any halfway competent nonferrous smelting outfit can run it. Laterite ore refuses this treatment. Low nickel grades, high iron content, saturated with moisture. Pyrometallurgical processing burns through so much energy that the economics collapse. The only viable path to battery-grade nickel sulfate from laterite is HPAL: high pressure acid leaching.

HPAL deserves far more attention than it gets in most coverage of this topic, because its history explains why Indonesia’s dominance was not inevitable and why it could have easily gone the other way. The reaction runs inside autoclaves at 250°C and 40 atmospheres, in concentrated sulfuric acid. The autoclave lining must survive simultaneous high temperature, high pressure, and aggressive acid corrosion. On paper, HPAL has been “ready” since the 1990s. In practice, it destroyed capital for two decades straight.

High pressure acid leaching autoclaves operate under extreme conditions

Australia’s Murrin Murrin project is the case that anyone in the nickel industry over forty will bring up when HPAL comes up at a conference bar. The project was backed by the predecessor entity of Andrew Forrest’s mining empire, and it became a kind of rolling catastrophe in slow motion. The autoclave linings corroded faster than the engineering models predicted. Not by a little. The acid recovery loop broke down repeatedly. The design called for a specific throughput rate that assumed a steady-state acid balance; the actual ore variability made steady-state impossible during the first several years. The project swallowed round after round of additional capital. Engineers who worked on the Murrin Murrin ramp-up in the early 2000s talk about it the way combat veterans talk about a bad deployment: a lot of institutional knowledge about what not to do came out of it, and not much else. Papua New Guinea’s Ramu project went through its own version during ramp-up. Cuba’s Moa Bay, which had been running for decades, never consistently hit its design utilization rate. By the late 2010s, HPAL had a reputation in the mining finance community that was, to put it politely, terrible. Banks that had been burned on earlier HPAL projects were not writing new checks.

Indonesia broke through this wall. The mechanism was not Indonesian. It was Chinese hydrometallurgical engineering capability, moved to Sulawesi.

This part of the story rarely gets the specificity it deserves, so here is some. China’s nonferrous smelting sector spent the previous two decades processing every conceivable difficult ore body. The specific experience that transferred to Indonesian HPAL was not some single patented breakthrough. It was an accumulation of operational knowledge about how autoclaves actually behave when they are running at scale on variable feedstock. How fast titanium-clad steel liners degrade under specific acid concentration and temperature profiles. How to adjust acid dosing in real time when the incoming ore’s moisture content shifts between wet season and dry season loads. What the early warning signs look like when an autoclave gasket is about to fail, what the vibration pattern of the agitator shaft tells you about slurry density drift, how to manage the decantation circuit when the CCD thickener underflow solids percentage creeps up beyond design spec.

This knowledge does not exist in published literature. It lives in engineers’ field notebooks, in maintenance logs scrawled on workshop clipboards, in the reflexes of people who have personally opened a high-pressure autoclave after a failed run and diagnosed what went wrong by looking at the corrosion pattern on the liner.

Chinese companies moved this entire body of tacit knowledge to Sulawesi, paired it with Indonesian ore and cheap electricity, and completed capacity ramp-ups in two to three years that Australian and Canadian projects had failed to achieve in a decade. CNMC, Huayou Cobalt, GEM, and their partners did not possess some secret patented technology. They possessed enough engineers who had already run complex hydrometallurgical plants under chaotic real-world conditions, people who had instinctive responses to autoclave leaks, liner anomalies, and acid consumption spikes, and did not need to file a report to headquarters before acting. Remove the Chinese engineering teams from the equation and Sulawesi goes back to being jungle and fishing villages.

Indonesia had tried an ore export ban before, in 2014, and reversed it in 2017 with little to show for the exercise. The 2020 ban produced completely different results because every other piece of the puzzle happened to be in position at the same moment. Chinese battery production was on the brink of explosive demand growth, with nickel consumption forecasts inflecting sharply upward. HPAL, after a decade of Chinese engineering iteration, had finally crossed the threshold of commercial viability. Chinese capital, after five to eight years of Belt and Road groundwork, already knew the Indonesian investment landscape well enough to move fast. These preconditions converged around 2020 and the export ban was the trigger.

Autoclave lining must survive simultaneous high temperature, pressure, and acid corrosion

What followed rearranged the global nickel market. Indonesian HPAL capacity roughly doubled every year from 2021 through 2024. Enormous volumes of low-cost battery-grade nickel flooded into a market that had been structured around much higher-cost supply. The London Metal Exchange’s nickel short squeeze in early 2022, when prices briefly exceeded $100,000 per ton and the exchange was forced to cancel trades, exposed just how fragile the global nickel pricing system had become. That crisis accelerated the stampede by battery companies to lock in Indonesian supply through long-term contracts. Then, from late 2023 into 2024, the full wave of new Indonesian capacity hit the market simultaneously, and nickel prices crashed to around $15,000 per ton.

This price destruction accomplished something that no diplomatic initiative or trade policy could have: it made high-cost nickel mining uneconomic across most of the rest of the world. BHP suspended portions of its Western Australian nickel operations. Multiple producers in French New Caledonia fell into financial distress. Canadian nickel development projects were shelved with no target restart date. The competitive landscape did not diversify. It consolidated. The battery industry’s dependence on Indonesian nickel deepened at the exact moment when supply chain diversification was supposed to be the strategic priority. Indonesia did not use political coercion to destroy its competitors. It released low-cost supply and let market pricing do the work.

One more layer under the HPAL story. MHP, mixed hydroxide precipitate, is emerging as an alternative processing route with lower capital expenditure and shorter construction timelines. MHP produces an intermediate product less pure than HPAL’s direct nickel sulfate output, which must be shipped elsewhere for final refining. “Elsewhere” means Guangxi or Fujian province in China. Nickel products stamped “processed in Indonesia” may have completed only initial enrichment on Indonesian soil, with the battery-grade purification step happening in a Chinese refinery. The gap between label and reality is wider than the headline statistics suggest.

Sodium-ion batteries. If energy density crosses 200Wh/kg and reaches volume production within three to five years, demand for nickel in the low-to-mid-end EV and energy storage segments contracts. Indonesia has wagered tens of billions of dollars of HPAL and smelting investment on a future where nickel demand keeps growing. Battery chemistry evolution does not follow predictable trajectories. It lurches. Sodium-ion is still below the threshold, and the gap is closing. Indonesia’s bet probably pays off, because sodium-ion is unlikely to mature fast enough to dent the high-end NMC market where nickel consumption per kWh is highest, and because even in a scenario where sodium-ion takes a chunk of the low-end, the absolute volume of nickel demand from the remaining high-end applications still grows. But “probably” is doing a lot of work in that sentence.

Chinese Capital Needs a New Mailing Address

The nickel story explains Indonesia. It does not explain why battery factories are also going up in Thailand and Vietnam. The mechanism there runs through trade law.

The U.S. Inflation Reduction Act, passed in 2022, imposed battery supply chain localization requirements of a severity that caught the industry off guard. Starting from 2024 or 2025, any vehicle using battery components from a “Foreign Entity of Concern” loses eligibility for the $7,500 federal tax credit entirely. The definition covers any entity where the Chinese government or party holds 25% or more equity or control. Every major Chinese battery company qualifies. Exporting directly from China to the United States means the OEM customer forfeits $7,500 per vehicle. No automaker will absorb that.

The European Union is applying pressure from a different angle: the Battery Regulation’s supply chain due diligence requirements, mandatory carbon footprint disclosure, anti-subsidy investigations against Chinese EVs.

Chinese battery companies looked at their options. North America was tested. CATL’s partnership with Ford on a Michigan plant ran into ferocious political opposition in Congress and was restructured into a technology licensing arrangement. Signal received. Europe is being pursued, BYD in Hungary, CATL in Germany, but European electricity prices, labor costs, and construction timelines are punishing. Southeast Asia is what remains, and it happens to be good.

ASEAN trade corridors reach markets no single China or North America location can access

A factory in Thailand, Vietnam, or Indonesia stamps “Made in ASEAN” on every product leaving its dock. That label opens trade corridors toward Japan and South Korea via RCEP, toward the EU via bilateral agreements like EVFTA, toward India via the ASEAN-India FTA. No single manufacturing location in China or North America can access all of these corridors at once.

The trade rule mechanics: RCEP and AFTA rules of origin operate on a “substantial transformation” principle. The battery supply chain from precursor to cathode material to cell to module triggers a change in HS code classification at each step. A supply chain distributed across three ASEAN countries can qualify for ASEAN origin on the final product even if the upstream raw material starts in China, as long as each step meets its determination criteria. Treaty shopping amplifies this. The same product exported to Japan goes through RCEP, to the EU through EVFTA from Vietnam, to South Korea through whichever agreement offers better terms. Some Chinese battery companies have embedded dedicated rules-of-origin legal teams within their Southeast Asian operations, parsing each agreement clause by clause, computing optimal routing. This is fully compliant within the current framework, and the space for maneuvering is wider than most outsiders imagine.

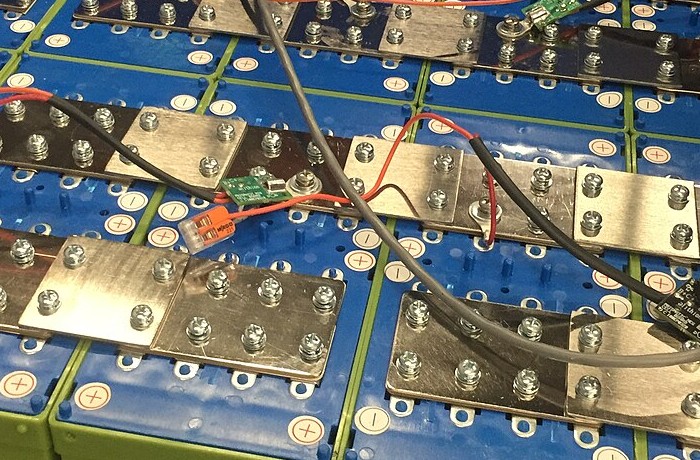

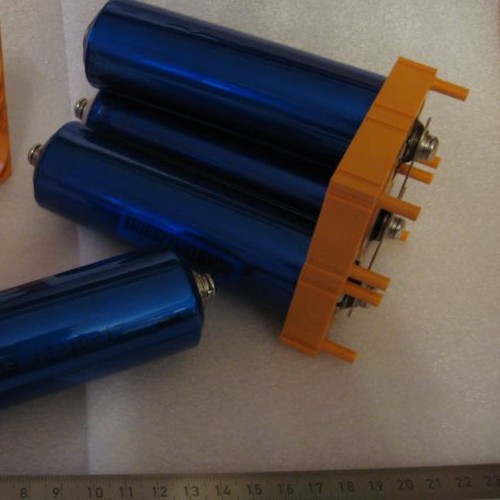

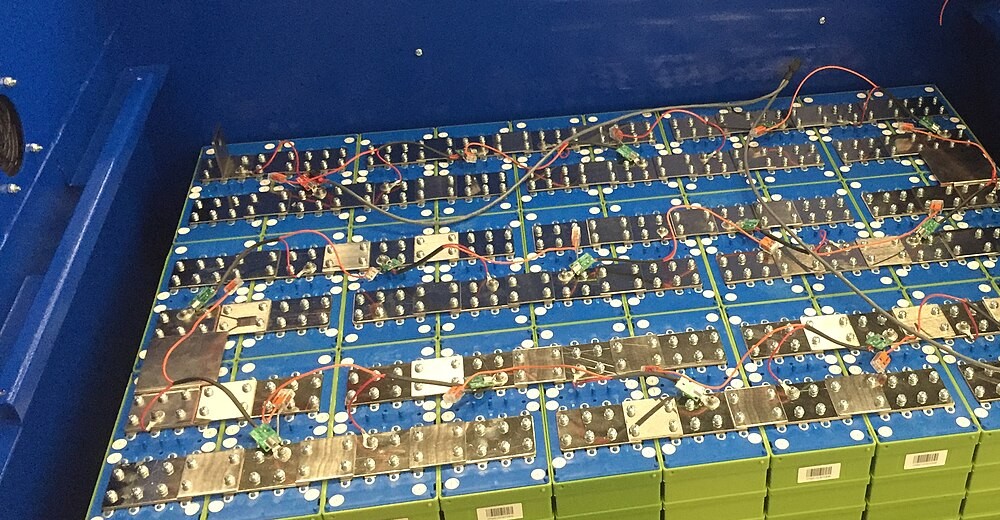

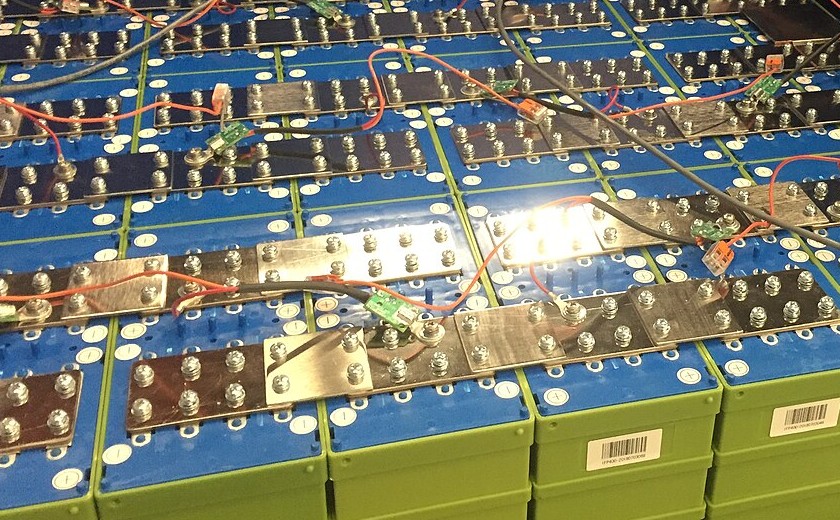

A point that matters and keeps getting lost in GWh headline numbers: a significant share of Southeast Asian “battery factories” are performing PACK assembly, not cell manufacturing. PACK assembly means importing finished cells from China and completing module arrangement, welding, BMS integration, and thermal management assembly locally. The technical barrier and value-add of PACK assembly sit an order of magnitude below cell manufacturing, which encompasses slurry mixing, electrode coating, calendering, slitting, winding or stacking, electrolyte injection, formation, and grading. Media reports almost never break down how much of a facility’s stated GWh capacity is cell manufacturing versus post-import assembly. The two are not comparable.

The knowledge control dynamics inside these factories matter more than the capex numbers. Chinese battery companies enforce strict compartmentalization of core process parameters at their Southeast Asian subsidiaries.

Coating line speed, NMP solvent recovery rates, electrolyte additive formulations, charge-discharge curve parameters in the formation protocol: access restricted to Chinese engineering teams rotated in from headquarters on three-to-six-month cycles. Local employees operate within preset SOP boundaries. The parent company spent billions in R&D and over a decade of experimentation to arrive at these parameters. Sharing them freely at an overseas subsidiary would be commercially insane. The arrangement is rational for the parent company and constraining for the host country, and everyone involved understands this without discussing it.

Japanese capital is entering Southeast Asia’s battery chain on a slower timeline. JBIC and JETRO have been facilitating Japanese battery material companies’ entry into the region. Sumitomo Metal Mining has operated a nickel-cobalt hydrometallurgical project in the Philippines for decades, building laterite processing experience long before the current Indonesian boom. Panasonic and Toyota’s joint battery venture can plug into supplier networks and government relationships that Japanese companies have cultivated in the region for half a century.

Thailand and Vietnam, Briefly, Because the Differences Are Simpler Than They Look

Thailand has no nickel, no lithium, no cobalt. It has thirty years of automotive contract manufacturing for Toyota, Honda, Mitsubishi, and Ford, and the entire supplier ecosystem that came with it. Battery PACK housings require aluminum die-cast or stamped steel components with precision tolerances similar to automotive body structural parts. The Tier 2 suppliers in Rayong and Chonburi that have been making automotive stampings for decades can pivot to battery housings by adjusting tooling and process parameters, without buying new primary equipment. Laser welding and ultrasonic welding rigs for battery module tab welding share the same equipment platform as automotive wire harness terminal welding. Operator retraining takes weeks. This accumulated support infrastructure is Thailand’s hardest-to-replicate asset because it cannot be fast-tracked. Vietnam can build a battery assembly plant in three years. It cannot conjure two hundred specialized supporting suppliers around that plant.

Thailand’s three decades of automotive manufacturing infrastructure

Thailand’s grid is the most stable in Southeast Asia. Cell formation requires continuous, precise charge-discharge cycling of each cell over days to weeks. A formation workshop on a 5GWh line has hundreds of thousands of cells online simultaneously. One grid interruption can cause uneven SEI film growth across an entire batch. Mild cases get downgraded. Severe cases are scrapped. Losses from a single power outage run into the millions. Cell manufacturers treat grid reliability as non-negotiable in site selection, and Thailand is the only Southeast Asian country that meets the threshold. This is not a marginal consideration. It is the primary reason genuine cell manufacturing gravitates toward Thailand while smelting and material processing concentrates in Indonesia.

Thailand’s EV purchase subsidy scheme has a structural fragility: subsidies are disbursed before factory commitments are verified. Several Chinese automakers collected subsidies while selling imported vehicles, pledging future factory construction. In 2025, postponement signals appeared on some of those timelines. Thailand’s Ministry of Industry faces a choice between enforcing penalty clauses and risking investment relationship damage, or exercising leniency and undermining policy credibility. This is playing out now.

Precision assembly capability in Southeast Asian manufacturing clusters

Vietnam’s position in the Southeast Asian battery map is narrower than it appears in most coverage. No mineral resource upstream. No thirty-year automotive supplier cluster midstream. The segment Vietnam can credibly occupy is precision assembly of battery modules and PACKs. Samsung’s factory complex in Bac Ninh and Thai Nguyen has trained over 100,000 workers in cleanroom discipline and micrometer-level assembly, and the skill overlap with battery module assembly is high. That is a legitimate advantage for that specific segment.

VinES, VinFast’s battery subsidiary, has announced plans for in-house cell production. Building cell manufacturing capability from scratch, without a parent company’s accumulated process knowledge, requires navigating the 12-to-24-month ramp-up between line commissioning and yield rate stabilization above 90%. For a company without prior cell manufacturing experience, that period extends. As of now, the evidence tilts firmly toward Vietnam remaining an assembler.

EVFTA gives Vietnam preferential tariff access to the EU market. The approaching EU Battery Regulation carbon footprint disclosure requirements threaten to erode this advantage. Vietnam’s electricity mix has a high coal share. If the EU sets strict enough carbon footprint ceilings, Vietnamese factories could find tariff preferences and carbon compliance pulling in opposite directions.

Process Knowledge

There are fewer than twenty engineering teams on Earth that can independently run a cell production line from end to end. All of them are in China, Japan, or South Korea.

The piece of this chain that resists documentation most stubbornly is coating process window determination. Coating requires depositing cathode or anode slurry onto copper or aluminum foil at extremely high thickness uniformity. Slurry solid content, viscosity, and thixotropy couple with coating speed, doctor blade gap, and drying temperature profile in relationships that are nonlinear and sensitive to feedstock variation. The optimal parameter set is not computed from first principles. It is converged upon through hundreds of trial runs and failure analyses of rejected electrode sheets. An engineer with a decade of coating experience can look at an electrode sheet surface and diagnose slurry formulation issues by sight. That diagnostic reflex does not transfer through written procedures. This is what makes the talent gap so stubborn, and why Southeast Asian universities starting battery programs now will not produce usable graduates before 2030 at the earliest. The gap between capacity expansion and talent development is widening.

Southeast Asia’s battery production lines exist physically. The knowledge that determines whether those lines produce cells at 60% yield or 95% yield remains stored in the heads of rotating Chinese and Korean engineers.

When those engineers leave, the line keeps running on the parameters they set. If something goes wrong that falls outside the pre-programmed SOP response, the local team calls the home office. This is the state of things.

Cell production process knowledge resides in tacit engineering expertise

What Could Change

Dry electrode technology eliminates the NMP solvent and the massive drying ovens that follow coating. Cell manufacturing energy consumption drops hard. Electricity price differentials shrink in importance as a site selection factor. Southeast Asia could benefit. Every traditional wet-coating line currently under construction in the region becomes a stranded asset candidate if dry electrode matures before those lines reach end of equipment life. The bottleneck is electrode sheet thickness uniformity under solvent-free processing. No one has cracked it at production scale yet, and “yet” is doing uncertain work there.

Solid-state batteries, if they reach mass production in the 2030s, share almost nothing with current liquid lithium-ion production processes. Slurry mixing, coating, electrolyte injection either vanish or get replaced by fundamentally different unit operations. All solid-state manufacturing know-how currently sits in R&D labs in Japan, South Korea, and China. Southeast Asia has zero presence.

Battery recycling infrastructure in Southeast Asia is essentially nonexistent. The EU Battery Regulation has set minimum recycled content requirements for future battery products. China already has a mature recycling industry. Southeast Asia is blank. This will not matter for five years. It will matter enormously at the ten-year mark.

DSTP, deep-sea tailings placement, is the cheapest disposal method for HPAL tailings and is being used or planned at several Indonesian operations. Volvo and BMW have flagged nickel supply chain environmental compliance as a procurement criterion, and this shows up on supplier audit scorecards, not just in press releases. If DSTP-sourced nickel gets excluded from approved supplier lists by European OEMs, affected processors face a choice between losing European customers and building parallel production lines with land-based dry stacking at significantly higher operating cost.

Technology shifts could reshape the competitive landscape within a decade

Adding It Up

Three forces stacked at the same moment around 2020: Indonesia’s nickel endowment combined with the HPAL technical breakthrough, Chinese battery capital’s need for a non-Chinese export identity under FEOC and EU pressure, and ASEAN’s multilayered trade agreement architecture. The window would not have opened earlier because HPAL was not commercially reliable, the IRA did not exist, and Chinese battery capacity had not yet overflowed. It may not open again because the competitive nickel landscape has already been permanently reshaped, trade rules may tighten to close origin-restructuring pathways, and Southeast Asia’s industrial land and power supply margins are being consumed fast.

Southeast Asia has gained production capacity, employment, and export statistics. It has not gained process design autonomy or materials R&D capability. These factories execute instructions that originate in Shenzhen, Ningde, Seoul, and Osaka. Changing this requires R&D spending and a talent pipeline, both of which take a decade-plus to build and neither of which has started.